There is a fascinating article in today’s Wall Street Journal in its quarterly “Investing In Funds & ETFs on page R3.: The Time to High-Beta?

Once a Quarter.

The thesis is that new research conducted says that: “high -beta stocks tend to outperform in just one week per quarter. Only in that week, therefore, does it make sense that traders bet on high-beta stocks. That week occurs in the quarterly earnings season.

The article goes on to that to test the theory, one would invest, during the first week of earnings season in a high-beta stock ETF while shorting an equal dollar amount of a low ETF.

Their example in the article regarding a high-beta fund is the Invesco High Beta ETF. (SPHV) That ETF contains the 100 highest beta stocks of the S&P 500 index. The 100 selected have the “highest sensitivity to market movements, or beta, over the past 12 months. The fund and the index are rebalanced and reconstituted quarterly in February, May, August, and November.”

The example of low beta is the Invesco S&P Low Volatility ETF(SPLV) which contains 100 S&P 500 stocks with the lowest realized volatility over the past 12 months. It then weighs each stock based on its volatility(well, lack thereof).

I assume it is rebalanced every month, but was unable to speak to anyone at Invesco to give me that information.

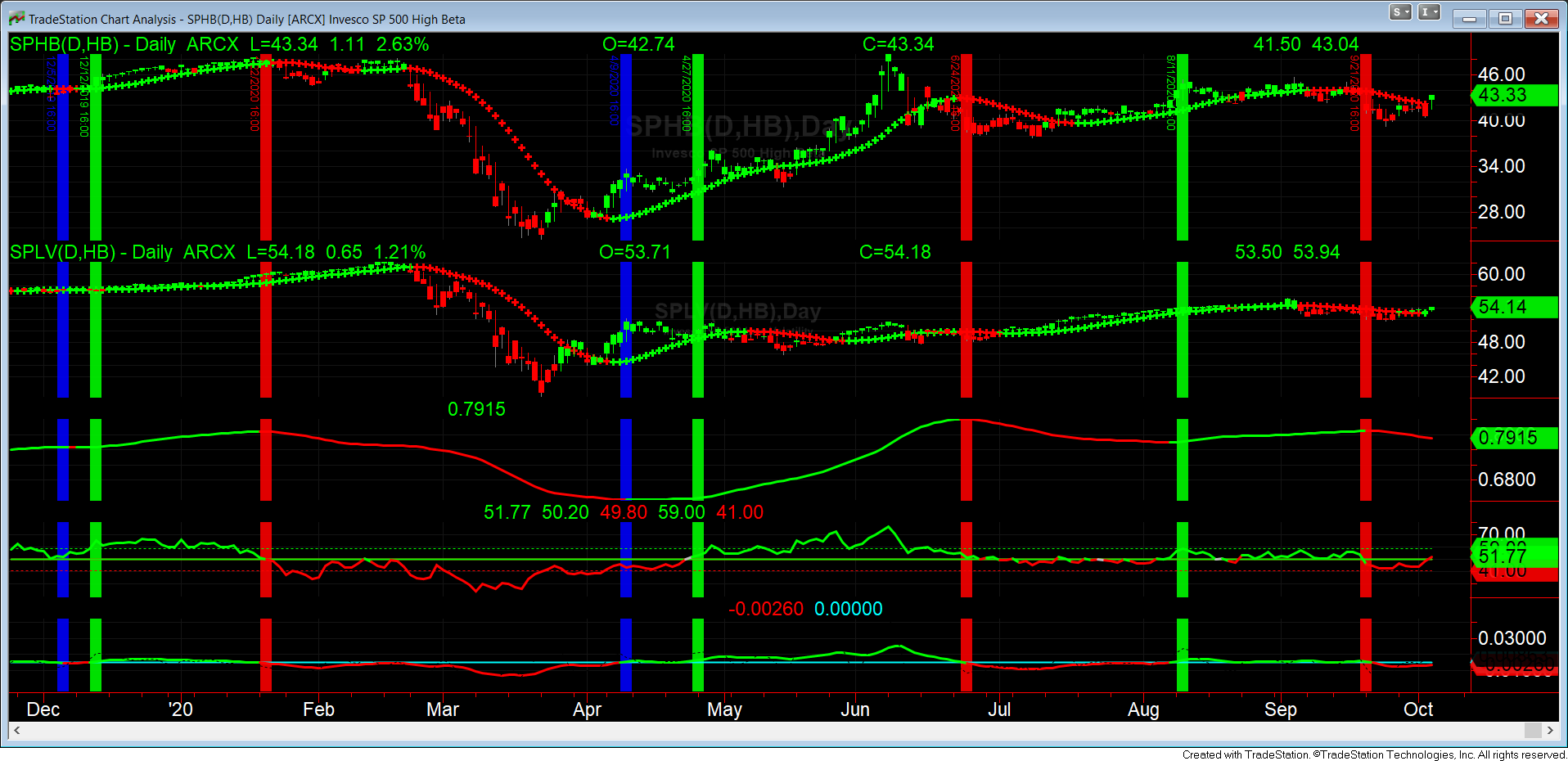

The article begs the question of whether a strategy of ALWAYS having a position in being long/short SPHV versus the reverse in SPLV would be successful?

The following illustration says YES!

The green vertical lines indicate long SPHB and short SPLV. The red vertical lines indicate long SPLV and short SPHB.